The recovery has begun.

Summary

April was a month of continued incremental improvement in crypto markets. Tokens absorbed a series of significant shocks - major DeFi exploits, renewed geopolitical volatility, volatile oil prices, CLARITY uncertainty, and a brief BTC dip toward $74K - yet emerged with improving institutional flows, accelerating onchain activity in select verticals, and the most consequential regulatory momentum the industry has seen in years. As of this writing, BTC sits about $76K, ETH at $2130 and SOL at $86, flat on the month but still well off February 5th lows.

We believe the crypto market recovery is in motion. Tokens are well-off all-time-highs, but, beneath the surface, a base is forming: the assets and protocols with genuine utility and strong fundamentals are compounding, while alt tokens that live on promises and no substance are left behind. Product-driven founders are sowing the feeds of PMF, and TradFi is preparing for mass adoption.

Macro Backdrop

The geopolitical environment in April remained volatile from a headline perspective, but strong AI-driven earnings growth trumped all worries with risk asset marching broadly higher on the back of a historical earnings season.

The US imposed a naval blockade on Iran on April 13, intercepting dozens of vessels, after peace talks in Islamabad failed to end the broader Iran war, a conflict that has kept the Strait of Hormuz largely blocked since late February. Most recently, Pakistan has been mediating between Washington and Tehran, expressing hope that a breakthrough deal is imminent, as the Strait's effective closure continues to disrupt global energy supplies. Oil remains elevated, with CL1 trading over $100, much higher than the ~$70 level seen right before the start of the conflict.

But high oil prices are proving inconsequential in the face of a historic earnings season for US equities, driven by the US AI boom. That strength is beginning to filter through the economy as AI capex turns into data-center buildouts, boosting demand for semiconductors, servers, networking equipment, power infrastructure, cooling systems, and construction services. Still, the benefits are not being distributed uniformly: the earnings impulse remains somewhat concentrated in AI-exposed technology and infrastructure, while healthcare is down and consumer staples, real estate, and energy remain comparatively muted. As of this writing, with 91% of S&P 500 companies having reported, 86% beat earnings estimates with index-level aggregate YoY earnings growth rate of 28%! Technology stocks showed incredibly impressive growth, with EPS tracking for 51% YoY growth. For context, EPS growth at these levels, outside of post-recessionary recovery environments, is extremely rare.

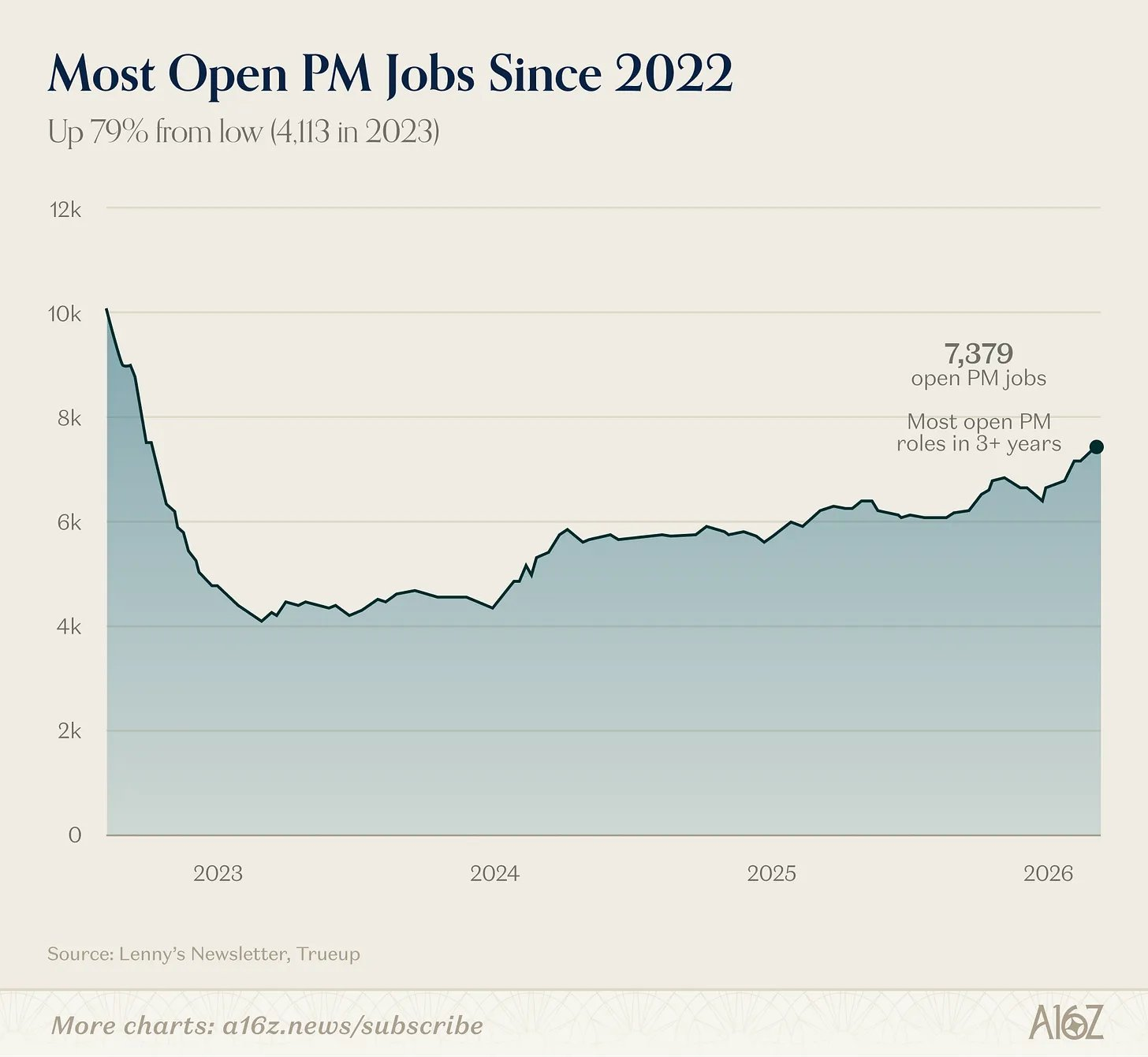

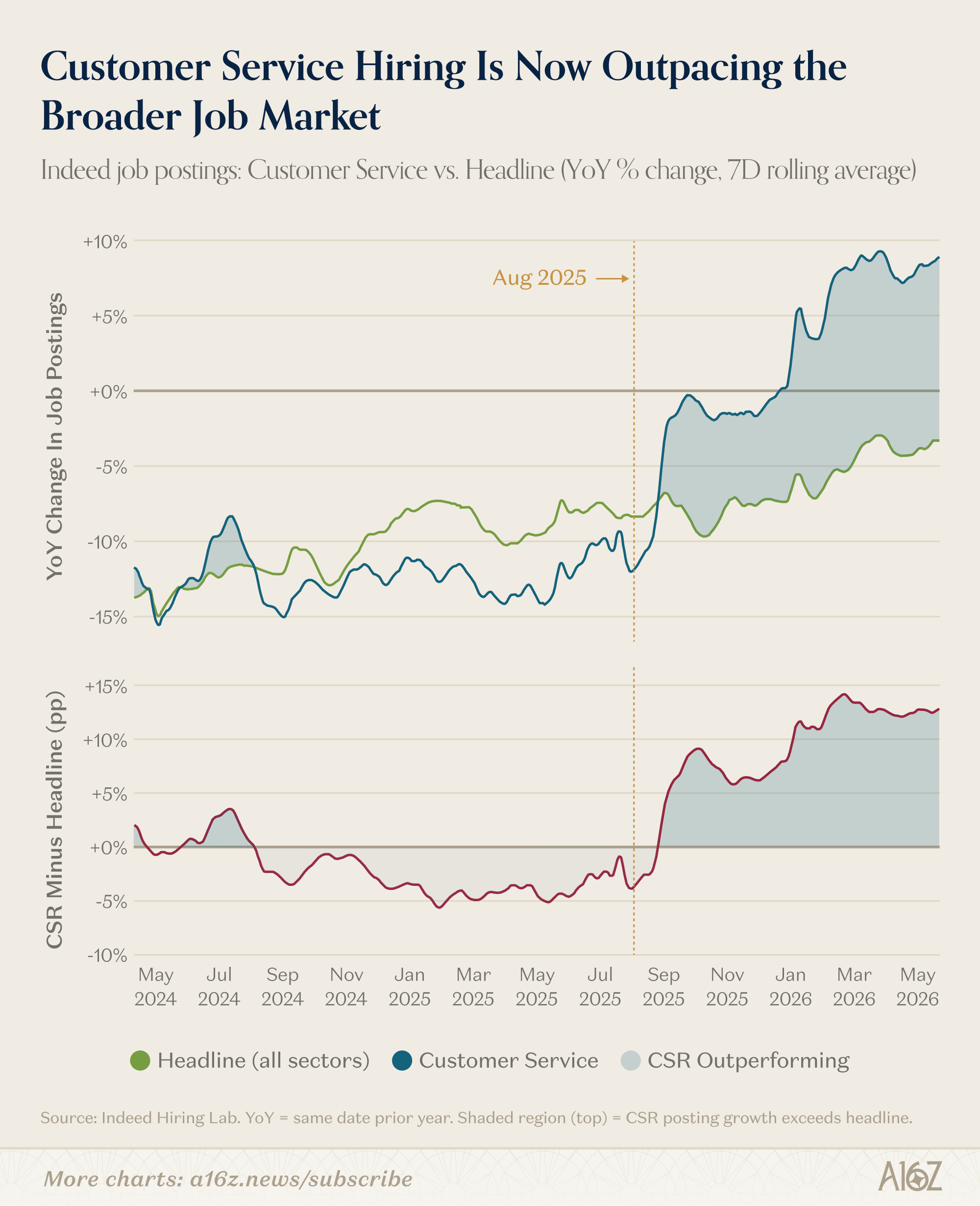

The US labor market continues to surprised to the upside. In April, 115,000 new jobs were added against an estimate of 65,000. Importantly, evidence continues to mount against AI-driven job loss fears. Software engineers, product managers, and customer service jobs - three areas assumed to be the first to be negatively impacted by AI - are actually doing the opposit. With software jobs now at the highest levels since 2022, and customer service hiring is now outpacing the broader job market. Additionally, broad unemployment, as measured by the U3 unemployment rate, seems to have peaked in October 2025.

US Core CPI printed slightly above consensus, but the market’s reaction was muted, though bond yields are generally at multi-month highs, with the US 30 year hitting highs not seen since 2007. We’re monitoring inflation risk. Generally, we believe higher oil prices would have to sustain well into 2026 and perhaps 2027 to impact growth and investor sentiment.

Technical Backdrop

As Bitcoin hovers around $76k, we look to certain technical momentum indicators to give us a read on trend & we’re constructive on what we see. The 20D MA has crossed the 50D, a sign of short-term strength. We’re also witnessing a visible uptrend being established in the 100D MA. The potential cross of the 50D over the 100D in the coming weeks could be a bullish catalyst for traders, which typically view this cross as an “all clear” to take more risk. These are not absolute signals however - we remain focused on both qualitative and quantitative market signals.

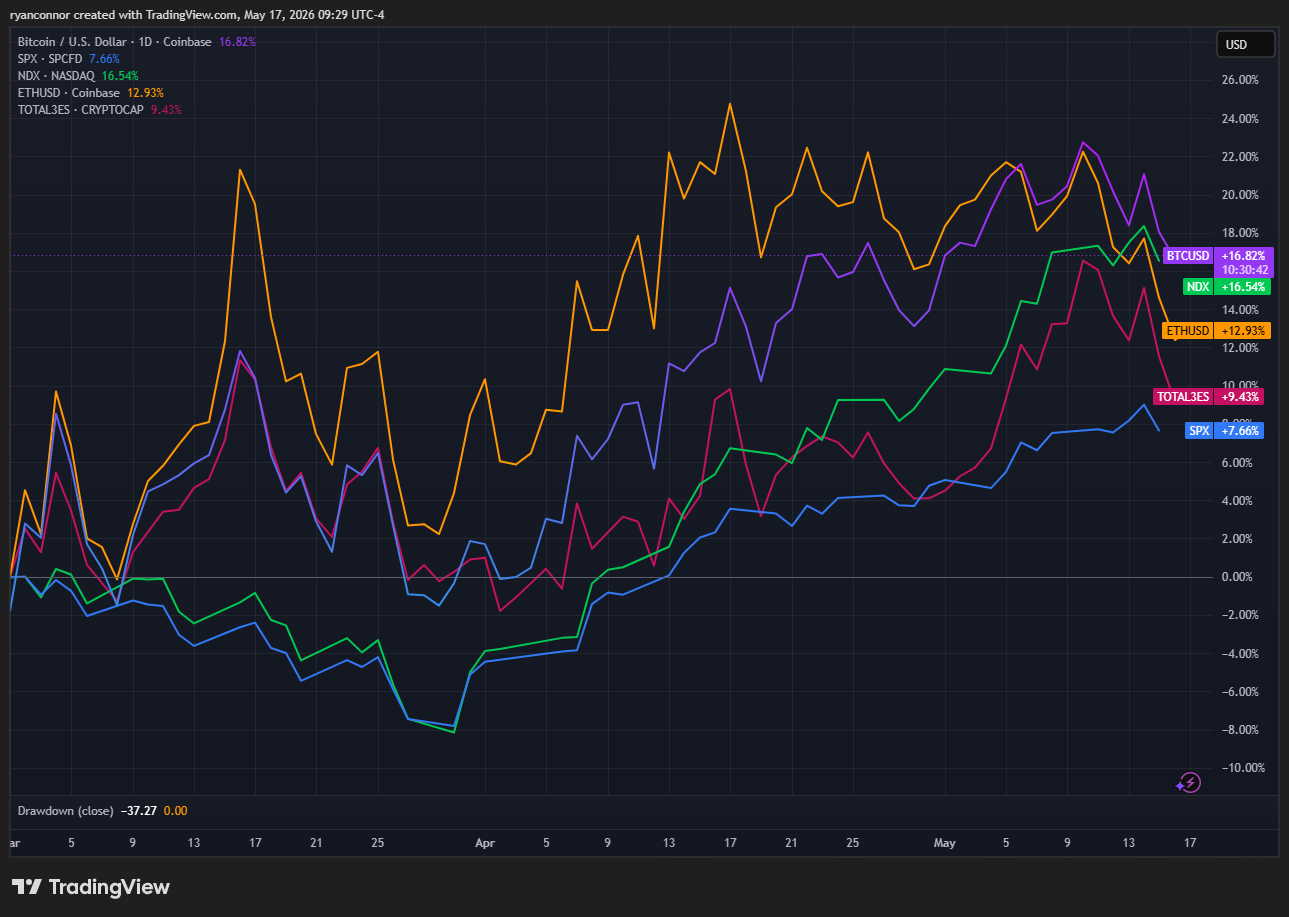

Despite recent volatility in May, BTC continues to outperform the Nasdaq since beginning of the US-Iran War, which we believe is a sign of strength, especially in the context of over $600M defi hacks in April (more on this below).

TradFi Flows

Supported by robust appetite for risk assets broadly, April marked the second month of meaningful re-engagement of institutional capital into crypto after a multi-month drought.

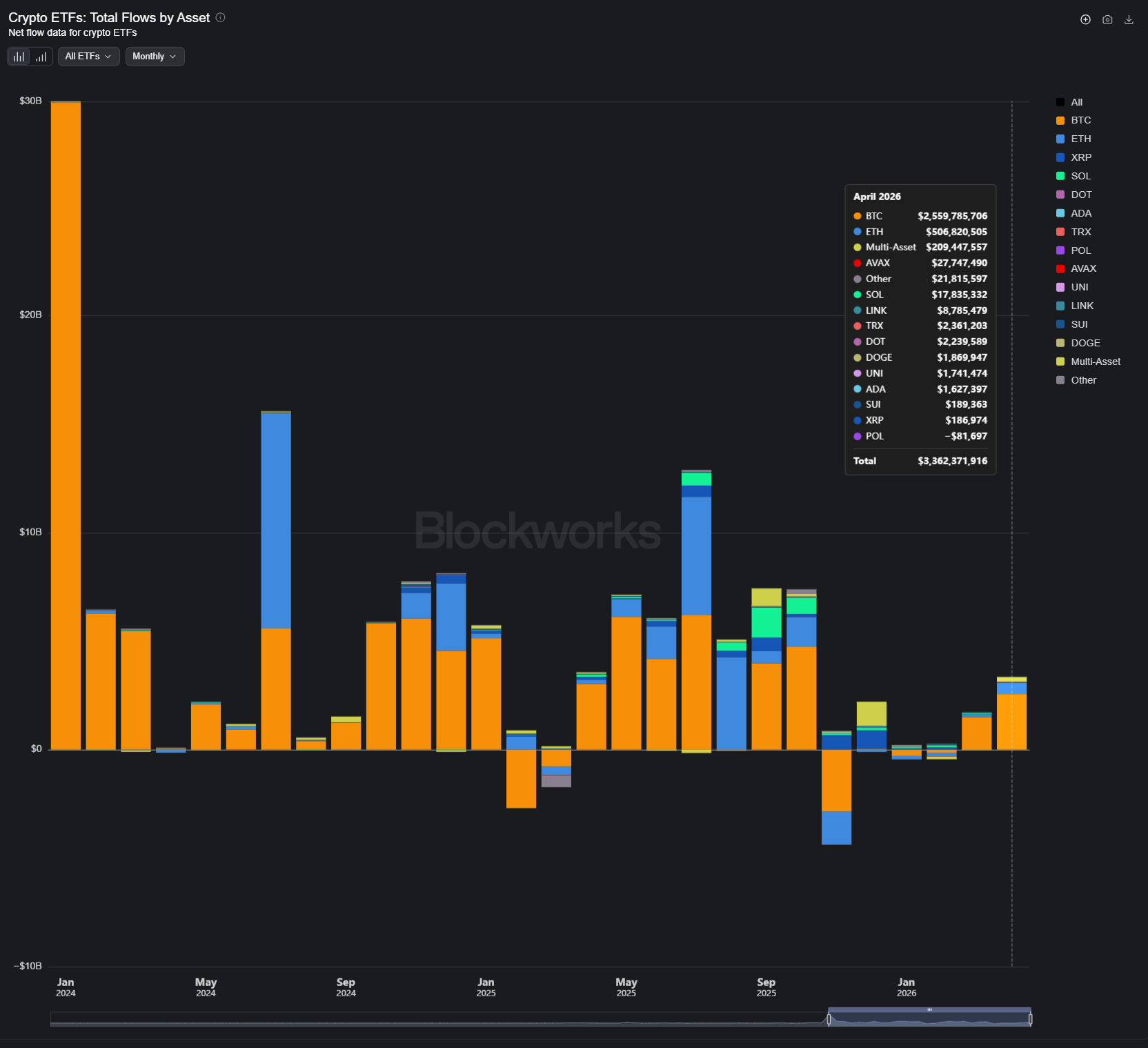

Total crypto ETF inflows reached $3.36B in April, the strongest monthly figure since October . BTC ETFs led with $2.56B in net inflows, continuing the recovery that began in March after months of outflows or near-zero flows in Q4 2025 and early 2026. We believe the signal here is clear: institutional allocators have reengaged, and BTC, for now, remains the preferred vehicle for exposure.

ETH ETFs amassed $506M in net flows, a meaningful recovery after the worst period on record (approximately $3B in outflows in November 2025) and several subsequent months of stagnation. This is the strongest ETH ETF month since mid-2025, and it comes despite the Kelp-Aave exploit creating a difficult backdrop for DeFi sentiment broadly. We believe the resilience of ETH flows in this context is noteworthy.

SOL ETF flows were modest in April at $17.8M, a step-down from their September 2025 peak of ~$1.4B. That said, positive-flow consistency, despite its relative lack of TradFi attention, remains a point of distinction for SOL among L1 assets.

Strategy made four Bitcoin purchases in April 2026, acquiring approximately 56,235 BTC for a total of roughly $4.13 billion, 2x more than BTC ETF flows, including its third largest ever single day purchase on April 20th. A portion of these purchases were funded through sales of the company's perpetual preferred stock, STRC, alongside common stock sold via its at-the-market (ATM) equity program.

Bitmine also continued purchases, accumulating 128,404 ETH since April 1 through mid-May. We continue to believe the highest quality DATs will drive flows to majors and be important stewards of the crypto ecosystem.

DeFi’s Resilience

The Kelp-Aave Crisis: Crypto Passes the Stress Test

The defining security event of April was the Kelp DAO exploit on April 18th. Attackers attributed to the Lazarus Group compromised KelpDAO's LayerZero bridge, which resulted in a $292M unauthorized mint (read: theft) of rsETH. Rather than selling immediately, the attackers deposited the unbacked tokens as collateral into Aave V3 and exploited its E-Mode framework to borrow approximately $193M in WETH.

The consequences cascaded rapidly. Because Aave is a monolithic architecture - all assets share one giant liquidity pool across many collateral types - losses and liquidity stress spread across the entire system, impairing depositors unrelated to rsETH. Modular systems like Kamino & Morpho isolate assets & risk into separate markets, so bad debt is contained to that specific market, and so lenders know precisely which risks they are underwriting. A degree of contagion is thereby mitigated.

The news triggered a run on Aave, amounting to Aave's worst weekly outflow on record at roughly $8.7B, pushing WETH utilization to 100% and effectively freezing liquidity for remaining depositors. Stablecoin markets followed, with popular markets like USDC, DAI, USDT, USDe markets all pinned at 100% utilization for days. This was an truly unfortunate event for the Kelp and Aave teams, and also defi at a large.

However, the most important takeaway from this events was crypto’s resilience. Despite a bank run of historic scale, during a month of similarly large defi hacks, defi tokens held their experience major losses, and the market continued to steadily grind higher.

This, in isolation, is bullish. When markets shrug off bad news, it’s a sign that selling pressure has been fully exhausted, or the the market can absorb negative catalysts without breaking down, implying bid is structurally strong.

For our portfolio companies Morpho & Kamino, April's events were a vindication of their market design choices. The modular architecture offers the risk isolation that Aave's monolithic pool cannot. As such, no Kamino or Morpho depositors were not impacted by bad debt.

Onchain: What's Working

Onchain data in April tells a two-track story. Broad DeFi sentiment was rattled by a significant exploit, but specific verticals such as onchain equity trading & consumer crypto continued to compound.

Solana: The RWA Trading Layer of Choice

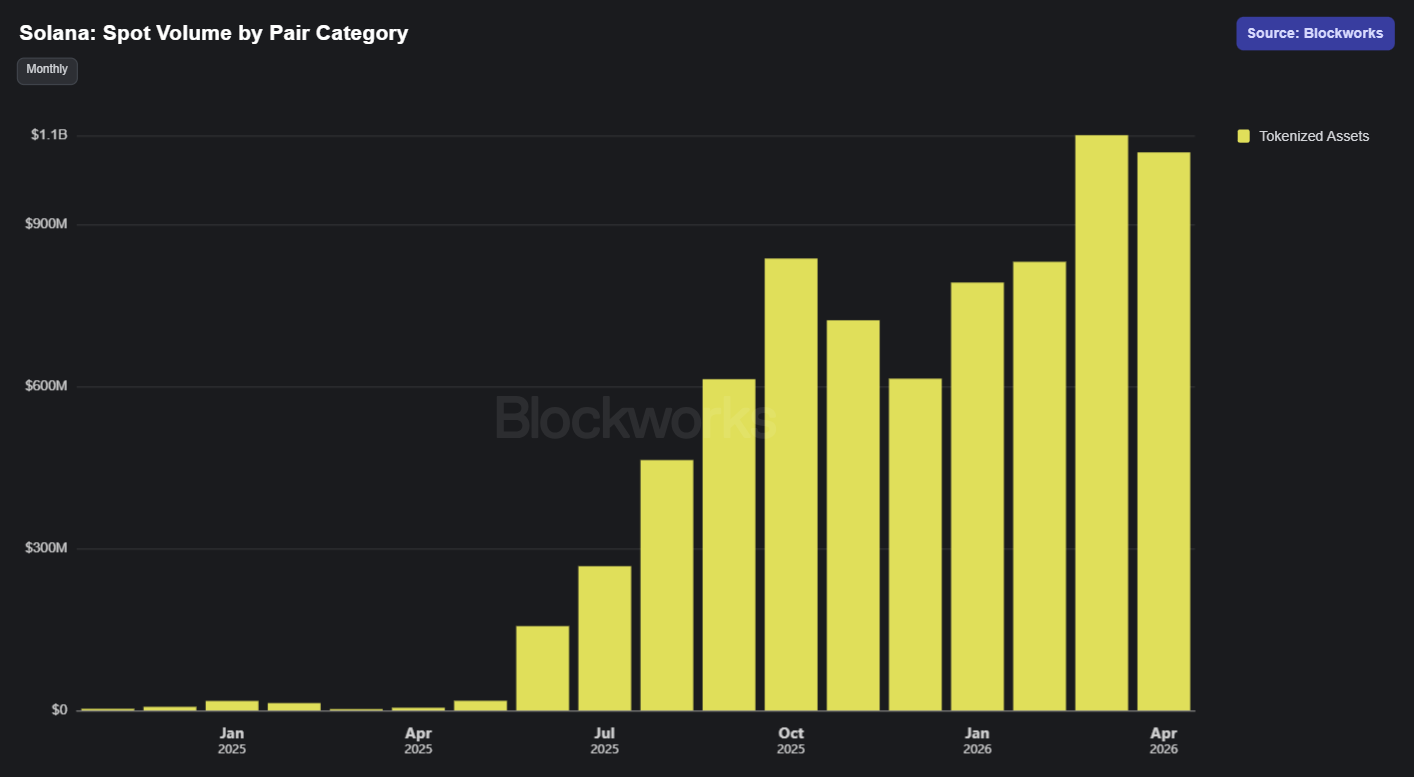

Solana achieved over $1B in tokenized spot asset volume for the second consecutive month, with equity trading on Solana reaching new highs of ~$680M in volume. We believe the rise of equity trading on Solana is a continued validation of the Solana thesis - the combination of low fees, fast settlement, deep liquidity, a large retail installed based, and a product-oriented developer ecosystem has made Solana the natural home high turnover / high revenue financial market activity. Spot equity trading, we believe, will continue to naturally migrate to Solana.

Consumer Crypto: Under-appreciated Growth

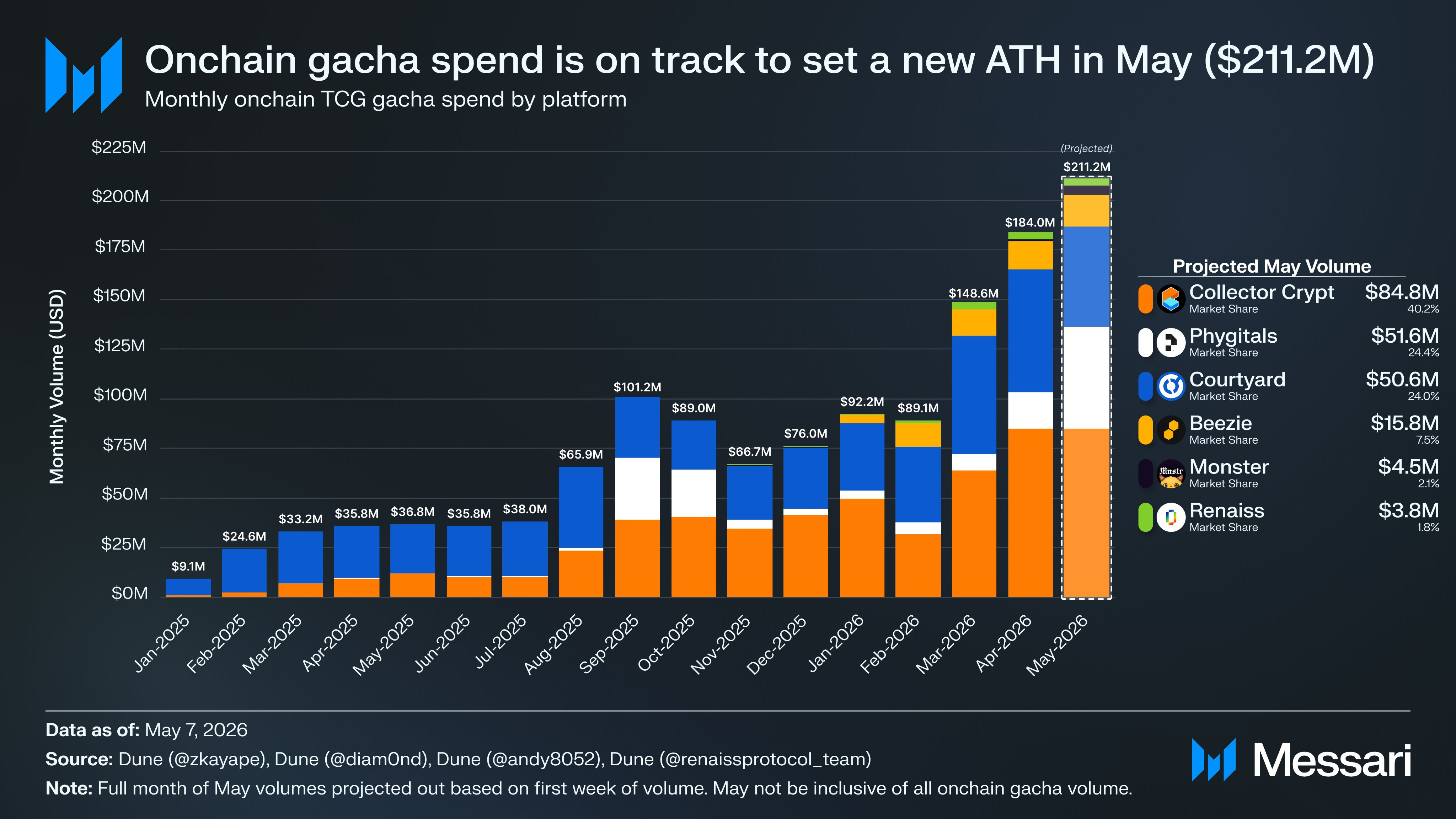

While institutional attention has focused on stablecoins and RWAs, a genuine consumer crypto economy is quietly compounding. Monthly onchain TCG (Trading Card Game) gacha spend - spend on randomized digital card-pack openings - reached $184M in April and is projected to hit a new all-time high of $211.2M in May - representing approx. 23x growth since January 2025.

This is a category that barely existed 18 months ago. Today it is a $2B+ annualized market, and it is growing entirely independently of price action in BTC or ETH. We believe this vertical remains significantly underappreciated by institutional allocators. We are in close contact with builders in this space and are watching the sector closely for opportunities.

Closer to CLARITY

April's regulatory story is straightforwardly constructive, and May is delivering on the momentum.

The biggest recent development is that the U.S. Senate Banking Committee advanced the CLARITY Act with a 15-9 vote on May 14, moving it out of committee and toward a full Senate vote. The bill would create a broad federal crypto market structure framework, clarify SEC vs. CFTC jurisdiction, define when tokens are securities versus commodities, and establish rules around DeFi, developers, stablecoins, and intermediaries. Most importantly, it would remove the regulatory uncertainty keeping investors and enterprises from fully embracing crypto markets.

A key breakthrough was a compromise on stablecoin “yield” provisions that had previously stalled negotiations between banks and crypto firms. The revised bill bans interest-like payments on idle stablecoin balances but still allows certain activity-based rewards tied to staking, liquidity provision, or governance.

The broader regulatory picture continues to compound positively. The GENIUS Act's stablecoin framework requires final implementation rules by July, 2026. Perps legalization in the US, as signaled by the CFTC in March, remains on track. And the Trump administration's reversal on AI regulation, with major AI labs now voluntarily submitting models to government review through CAISI, suggests a pragmatic approach to oversight and a positive backdrop tech markets broadly.

Closing Thoughts

We leave April with more conviction than we entered it, and note that the positive catalysts driving crypto market - favorable regulation, tradfi flows, onchain growth - continue despite recent volatility. What’s clear about 2026 thusfar, which is true of past drawdowns in crypto prices, is that volatility has been an opportunity for long-term investors. We believe this has been the case this year, and remain excited for what’s ahead.