Crypto has always been looking for better ways to fund new ideas. From the ICO mania to today's launchpads, the dream is the same: permissionless, fair, early-stage, and aligned with what actually gets built. But despite all the innovation in liquidity tech and token issuance, most fundraising still looks a lot like the Web2 venture pipeline — private rounds, low float, and public markets locked out until valuations are already sky-high.

Internet Capital Markets (ICM) emerged on Solana as a broader thesis: open, on-chain issuance paired with continuous trading and governance for internet-native assets. The novel fundraising mechanisms I'm covering here — structured on-chain capital formation tools — are one piece of that thesis, not ICM itself. ICM is the full stack: issuance, trading, governance, community participation. What we're looking at is the capital formation layer within that bigger picture.

The idea is simple enough. Instead of raising through sequential VC rounds, founders tap global markets directly. Communities get real governance power, not just bags to speculate on. In practice, though, most of what's shipped under the ICM banner has been messy — inconsistent governance, unclear value accrual to tokens, incentives that don't line up between builders and holders. These systems do expand access compared to traditional venture capital, but nobody has nailed a unified model for early-stage on-chain capital formation. Not yet, anyway.

Two platforms have emerged as the serious contenders in this space: MetaDAO and Metaplex Genesis. MetaDAO is the market leader — it goes further than anyone else in tying issuance, treasury control, legal structure, and market-driven governance into one integrated system. Metaplex Genesis takes a different angle, solving the technical infrastructure side of fair token launches. Both matter, but they're doing fundamentally different things.

The Fundraising Landscape

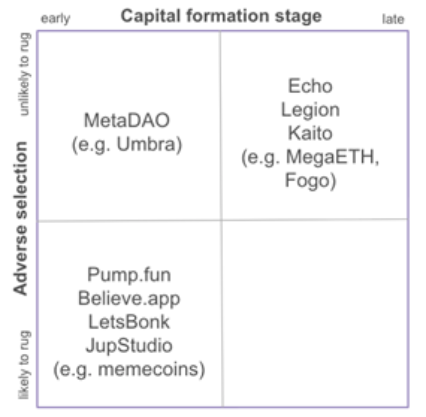

Today's crypto fundraising tools fall into two buckets that almost never talk to each other. The tradeoff is between adverse selection and valuation — platforms that are easy to launch on tend to have high adverse selection and low valuation. This tradeoff is visualized below:

Permissionless Issuance (Believe / Launchcoin and similar)

These are the most frictionless rails out there. On Believe, you reply to an X post and a bot deploys a token contract with a bonding-curve market. No constraints on mint authority, no treasury rules, no governance.

The problem is obvious. When it costs nothing to launch, everything gets launched. Token holders have no rights. Founders can mint more tokens, walk away, or extract whatever they want. It's optimized for going viral, not for building anything.

Bonding-Curve Launchpads (Pump.fun, LaunchLab, LetsBonk, Meteora Launch Pools, Jupiter LFG, Raydium)

Tokens trade on a bonding curve first, then liquidity migrates to an AMM once a threshold is hit. No treasury commitments, no governance.

These platforms create tradable tokens, not organizations. They're technically solid for memecoins, but they don't support real fundraising in any meaningful sense. The propensity to rug — and the probability of getting rugged — are both through the roof. You're creating a token, not a business.

Curated Launchpads: (Sonar by Echo, Legion)

These reduce risk through curation, KYC, or compliance, but they concentrate control and shut out anything early-stage. Founders put up a sale page, users deposit stablecoins, tokens get distributed after the sale closes. Compliance happens off-chain.

The catch: founders and the platform control supply, pricing, and vesting. There's no on-chain governance. And because sales happen after PMF signals and private rounds, you're getting in at $300M–$500M FDV — basically late-stage venture pricing with a token wrapper.

Everything Else

Kaito Capital Launchpad does something interesting with reputation-weighted allocation based on X activity and on-chain history. But the scoring is opaque and off-chain, and there's no governance layer underneath.

CoinList, Tokensoft, and Republic Crypto are the fully regulated option — KYC/AML, custodial settlement, standardized vesting. High compliance, but no governance, no early-stage access, and high valuations. These are closer to IPO rails than anything crypto-native.

What's Actually Broken

Across all of these, the same problems keep showing up.

Token holders almost never get real rights. Governance is optional or toothless, treasuries stay founder-controlled, and tokens often capture very little of the project's actual economic value.

The adverse selection problem hasn't been solved. Open platforms are flooded with garbage. Curated platforms filter it out but only let you in after VCs have already priced the deal.

Float is too low and liquidity is unreliable. Late-stage sales launch with 5–10% of supply circulating. Early markets are thin enough to be easily manipulated.

And issuance, liquidity, and governance are all handled by different systems that don't share any assumptions. Nothing is integrated.

This is where MetaDAO and Metaplex Genesis enter the picture — two platforms that are trying to fix different parts of this stack in fundamentally different ways.

MetaDAO

MetaDAO is a fundraising and governance venue on Solana and the current market leader in structured on-chain capital formation. It runs "unruggable" token sales and TGEs, and uses conditional market-based decision-making — the "futarchy" concept — where proposals are decided by prices rather than token votes. No other platform on Solana integrates issuance, treasury custody, legal structure, and governance into a single architecture the way MetaDAO does.

The Fundraise

MetaDAO runs structured ICOs. Investors get four days to commit USDC. Founders set a discretionary cap, and allocations are pro-rata with refunds if you're over. Tokens go out at close. If the minimum isn't met, everyone gets their money back. Price is straightforward: discretionary cap divided by tokens raised.

Here's where it gets interesting. After a successful sale, all the USDC goes into a market-governed treasury — a multisig on Squads where the signer is the FutarchyDAO. Mint authority transfers to the treasury too. And 20% of the USDC plus 2.9 million tokens get deployed as liquidity, creating a mechanical buy-below/sell-above band around the offering price.

Teams can only draw a pre-configured monthly budget unless the market votes to give them more. Omnipair, for instance, passed proposal OMFG-001 to bump their allowance from $10k/month to $50k for additional hires. You have to ask, and the market has to say yes.

On the founder incentive side, teams can optionally set up a performance package — up to 12.9M tokens (half the initial supply) that unlock in five tranches at 2×, 4×, 8×, 16×, and 32× the offering price. There's a minimum 12-month lock and a TWAP check. To be clear: this doesn't mean founders get half the supply. It means they can configure a price-and-time-gated vesting pool. Big difference.

What "Unruggable" Actually Means

The treasury is mechanically unruggable. 100% of proceeds sit in a market-governed on-chain treasury. Nobody can just take the money and run.

Revenue is a different story. It's not locked the same way, but there is legal accountability. If a founder misappropriates revenue, or just walks away, or the price craters below book value, anyone can put up a proposal to return capital to holders. There's a legal entity created at launch, so token holders could actually sue teams that steal revenue, or force service providers to transfer IP to a new team.

TWAP-based manipulation guards help on the governance side — outcomes need to reflect sustained conviction, not a single block of spiking. Founder earnouts need sustained pricing above targets to unlock, not just a flash pump.

Governance

All governance is market-based. Proposals get listed as pass/fail markets. Outcomes are decided by a time-weighted average price — the pass side needs to clear a threshold above the fail side, which means passing is slightly harder than failing. That discourages last-minute manipulation.

Since November 2023, MetaDAO has processed over 90 proposals across more than a dozen organizations. Jito, Flash, and Sanctum have all used it. To propose something, you lay out your case — what you want to do and why — and the market reacts through the price.

Worth saying plainly: this is still risky for protocols. Markets can be shortsighted, thin, or just wrong. Some businesses genuinely need founder discretion for longer than token holders will tolerate. Futarchy is a better mechanism than token voting, but it's not magic.

How MetaDAO Makes Money

Two revenue streams. First, a 0.5% fee on Futarchy AMM volume. (This was originally split 50/50 between MetaDAO and projects, but since late December 2025 the full fee goes to MetaDAO.) Second, earnings from the protocol-owned liquidity MetaDAO deploys on Meteora alongside each launch.

This isn't theoretical anymore. Blockworks reported in early January 2026 that MetaDAO had pulled in roughly $2.4M since the Futarchy AMM went live on October 10, 2025 — about 60% from AMM fees and 40% from the Meteora LP. But the same report flagged that revenue was declining as launch cadence slowed. The model needs a steady flow of credible launches to work, not just good mechanism design.

As of March 2026, MetaDAO shows about $33.6M raised across 11 launches. That's real traction, but it's still a small sample. The product is being validated on a handful of teams, not across a deep long tail.

Metaplex Genesis

Metaplex Genesis is the other major fundraising mechanism on Solana, and it takes a very different approach from MetaDAO. Where MetaDAO builds the full stack — issuance, treasury, governance, legal entity — Genesis focuses on the launch infrastructure itself: audited smart contracts that make the token sale fair, transparent, and resistant to MEV snipers.

Genesis launched in July 2025 and supports multiple sale formats: launch pools (proportional distribution over a set window), presales (fixed price), and uniform price auctions (all bidders pay the clearing price). The platform charges a 2% protocol fee on deposits, and half of that revenue is automatically used for MPLX buybacks that flow into the Metaplex DAO treasury.

In February 2026, Metaplex shipped the Metaplex App — a no-code frontend on top of Genesis that separates project tokens (higher caps, longer windows) from memecoins (1-hour pools, lower caps). It also handles vesting, airdrops, and automatic 20% liquidity locks that migrate to Raydium. The Genesis SDK, released in December 2025, lets third-party platforms plug into the same infrastructure.

Genesis has had strong early results. Six ICOs through the platform have averaged 8.63× ATH ROI, with standouts like Collector Crypt (19.7×) and DefiTuna (9.7×). By October 2025, Genesis was contributing about 18% of Metaplex's total protocol revenue.

Where Genesis Falls Short

Genesis solves an important problem — fair, MEV-resistant token distribution — but it doesn't touch the parts of the stack that MetaDAO addresses. There's no market-governed treasury. Mint authority and treasury management stay with the project. There's no embedded governance mechanism, no legal entity wrapping the DAO, and no on-chain controls on how founders spend the money after the raise. Projects can configure vesting, but there's nothing stopping a team from controlling the treasury unilaterally.

Think of it this way: Genesis gives you a fair launch. MetaDAO gives you a fair launch plus ongoing accountability. Genesis is infrastructure — a set of composable, audited programs that any project or platform can plug into. MetaDAO is a venue — an opinionated system that makes specific claims about how the relationship between founders and token holders should work after the money is raised.

Both are useful. But if the question is "which platform does more to protect investors and align incentives over time," MetaDAO is ahead by a wide margin.

Futardio

Futardio is the permissionless version of the MetaDAO stack. It describes itself as a permissionless launchpad on Solana, and the project list is visibly wider and messier than curated MetaDAO. That's the whole point — and the whole risk.

What makes Futardio interesting is that it keeps the parts of MetaDAO that actually matter. Launch disclosures state that project IP, codebases, trademarks, and brands are held by a Cayman Islands SPC formed via MetaLeX and governed by the DAO. There's no separate dev company sitting outside the structure. The DAO treasury funds development directly through governance proposals. That's a much tighter link between the token and the operating business than the usual Labs/Foundation split.

But don't confuse this with equity. Futardio's legal terms are clear: ICO participants don't directly own the SPC or segregated portfolio. They aren't owed fiduciary duties. The legal wrapper is designed to respect decision-market outcomes, which improves alignment, but it's not the same thing as holding shares in a company.

The launch structure mirrors MetaDAO: 10M unlocked ICO tokens, 2.9M for protocol-owned liquidity, and a locked team package that only unlocks after a cliff and sustained price milestones. Insider incentives stay performance-linked, but public markets are evaluating the business from day one.

Ranger: The Stress Test

Ranger is the most important case study so far because it tested the downside path. MetaDAO's page showed $86.4M committed against a $6M minimum — about 14× oversubscribed. Huge demand. And the structure still blew up.

First came RNGR-001: a proposal to spend $2M of treasury buying back RNGR at NAV. The token had been trading at a deeper discount to book than other MetaDAO launches, which made the treasury a target for adversarial capital looking to force a liquidation.

Then came RNGR-002: "Liquidate Ranger Finance." It passed. The proposal argued the team had made material misrepresentations about the business and that a full unwind was the best outcome. Treasury USDC went back to unlocked holders based on a snapshot, liquidity was pulled, and IP went back to Glint House PTE. LTD.

This is the single most important thing about the whole mechanism. "Unruggable" doesn't mean the business is safe. It means token holders have a better claim when things go wrong. For investors, liquidation is a protection. For founders, it's a permanent constraint. If your token trades badly enough against book value, outside capital can buy in and vote to shut you down rather than wait for a turnaround that might never come.

Nothing like this exists on Genesis, or on any other Solana launch platform. The Ranger episode — from oversubscribed raise to buyback to liquidation — is the best evidence that MetaDAO's architecture actually works under stress, even when the outcome is ugly.

Risks

Liquidation risk is real. Ranger went from oversubscribed raise to buyback defense to full liquidation.

Adverse selection will get worse as the model goes permissionless. MetaDAO screens for founder quality. Futardio opens the door. Quality variance will widen.

Governance markets can still be thin. If launch cadence drops or trading depth is weak, decision-market prices get less informative and easier to game.

The legal wrapper helps, but it has limits. Token holders don't get equity rights. Regulatory treatment is unsettled.

Value capture is indirect. Fees and treasury assets sit inside governed structures. What META holders actually realize depends on future governance, not automatic distributions.

For Genesis specifically, the risks are more conventional: projects retain full control of treasuries and mint authority post-sale, so investor protections depend entirely on the team's integrity rather than on-chain enforcement. Fair launch mechanics reduce front-running, but they don't address the deeper question of what happens after the money is raised.

Why Any of This Matters

MetaDAO matters because it's pushing crypto fundraising away from the low-float, high-FDV, Labs/Foundation playbook that has dominated for years. It tries to make the token the real economic unit — tied to treasury control, IP ownership, and market-driven oversight from the start. That's a more serious approach to on-chain capital formation than anything else on the market, and it's one of the most tangible expressions of the broader ICM thesis.

Metaplex Genesis matters because it's building the infrastructure layer that makes fair launches composable and accessible. Not every project needs or wants full futarchy governance, but every project benefits from MEV-resistant distribution and standardized launch mechanics. Genesis is becoming the base layer that other platforms build on top of.

Together, they represent the two most credible paths forward for on-chain fundraising on Solana — but MetaDAO is the one making the stronger bet on what the full system should look like.

What Happens Next

I expect fundraising keeps moving toward token-first structures with stronger investor protections, but I don't think we end up in one fully permissionless equilibrium.

The more likely outcome is a layered market. Curated rails like MetaDAO keep attracting the best raises because they filter for quality and give investors confidence. Permissionless rails like Futardio grow as discovery and experimentation layers, but with more noise, more failures, and more adverse selection baked in. Infrastructure like Genesis sits underneath, providing the technical primitives that any platform — curated or permissionless — can plug into.

Investor expectations will keep shifting — toward higher float, clearer treasury and IP control, and explicit downside protections like buybacks, redemptions, and liquidation paths. The big open questions are liquidity depth, governance quality, and regulation. These structures are better aligned than the old model, but they're not simpler, and they're definitely not risk-free.

The future probably isn't "everything becomes Futardio." It's more likely that permissionless venues handle the experimental edge, infrastructure like Genesis handles the fair distribution problem, and curated, governance-bound structures like MetaDAO capture the strongest projects — the ones that want community capital without going back to the old insider-heavy token model.